There is a geographic disparity amongst the Citi Economic Surprise Index. Economies, both developed and emerging, are surprising to the upside in Asia and Europe while economies in the western hemisphere are not doing as well (at least in terms of meeting and exceeding expectations). Below we show some of the more interesting charts.

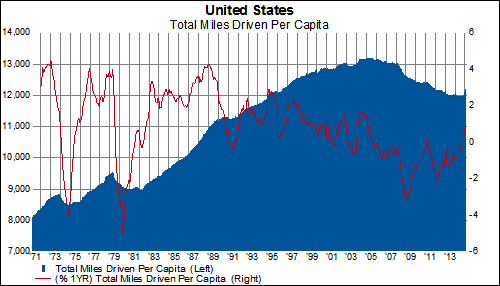

The second half of 2014 and the first month of 2015 (latest data available) shows a significant increase in total miles driven and total miles driven per capita. Total miles driven on an annual basis has reached an all-time high. The 2.12% year-over-year change is the largest YoY change in nearly 10-years (Feb 2005). And the one-quarter, annualized change (8.34%) is the largest increase since 1979.

Total miles driven adjusted for driving age population is still well below the all-time peak set in 2005. However, after a decade of steady declines, a "higher low" seems to be in place. The year-over-year change in total miles per capita is also nearly at a 10-year high. The one-quarter, annualized change is at its highest level since 1978.

Historically, there has been a fairly strong relationship in the trends of German construction output and the results of Markit's PMI Construction survey. However, yesterday's positive data release of the construction PMI painted a much different picture of the sector than today's release of industrial (and construction) ouput:

While this could be a temporary aberration, our interest is always peaked when survey or opinion data differ significantly from solid, fact-based numbers.

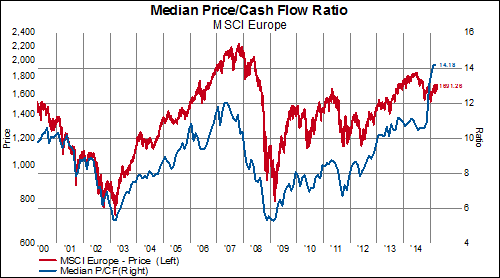

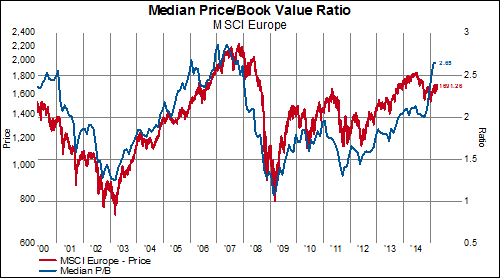

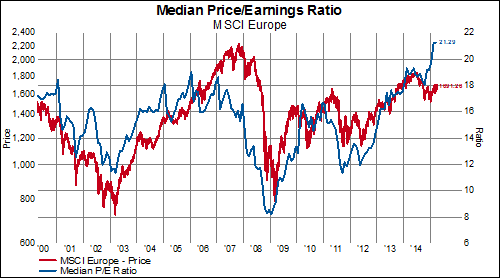

A month ago, we highlighted the continued trend of high valuations (P/CF in particular) for much of the developed markets. No region better illustrates the extremity of this trend than MSCI Europe. By any valuation metric, the recent surge in markets has driven constituents up to (P/B) or well above (P/CF, P/S, P/E) historic peaks:

Taken in aggregate, sector valuations in MSCI Europe currently trade at anywhere from a 20% to a 60% premium over the MSCI World average.

The story is the same when we look at valuations compared to their respective averages over the last decade-- European equities trade somewhere between 20-40% higher.

Taking a more granular look at the Industry Groups in Europe over the last ten years, we can see just how much P/CF valuations have expanded (red is high, green is low).

The last time valuations were even remotely close to being this high for the majority of constituents was in 2005/2006.

I often go back and re-read things that have shaped my perspective on managing portfolios. In my 20s (in the 1990s) I was fortunate to have a friend and mentor named Clay Allen who taught me volumes on the art of portfolio management. He introduced me to the point and figure method of charting stock prices and we often talked at length about how to win the "losers game".

Before his passing several years ago, he compiled many of his thoughts into a book titled Winning the Performance Game. One of his strongly held beliefs was to not be seduced into bottom fishing. According to Clay:

"Buying stocks that are suffering disastrous declines is often based on hope; hope that the market is wrong, hope that the problems really aren’t that bad, hope that the market is over-reacting to the bad news, hope that the stock price will go back up. The authors of BusinessThink remarked that hope was not an appropriate method for solving business problems. Hope, by itself, is also not an appropriate method for buying stocks. During the bull market, the strategy of buying the dips was rewarded handsomely but after the bull market ended, it became a loser. There seems to be a big difference between buying after a small dip and buying during a dramatic collapse in a stock’s price. Livermore said in Reminiscences of a Stock Operator, “It is perfectly astonishing how much stock a man can get rid of on a decline”. This thought indicates that, in Livermore’s day, the big traders could count on large numbers of bargain hunters to buy and, therefore, support the stock they were distributing. The desire for buying bargains incorporates an element of getting something for nothing, which often leads to investment disaster. It is also the basis of most criminally fraudulent schemes. This approach is often dressed up as contrary opinion, which is intellectually very appealing but difficult and dangerous to apply. Since there is always a buyer for every seller, how do we know to which side we are actually contrary? The stock market has a long history of extreme price movement, but how do we know what is an extreme until subsequent price action proves that it actually was an extreme? Until we get the proof, we can only hope that it was an extreme. Hope seems to be a flimsy basis for risking capital in the stock market. Many times, this bargain hunting mentality is encouraged by the idea of regression to the mean. The stock has dropped “too” much and it should recover to a more normal price. However, a statistician would argue that in the stock market, the tails of the distribution of returns are very fat. This means that a stock that is three sigmas below the mean could easily drop to four or five sigmas before recovering. In 1987, I was tracking a sample of 300 large- cap, active stocks that actually fell to seven sigmas below their relative strength mean in the crash. This was an event so rare as to be almost impossible, and yet it happened. In the war stories that came out after the crash of ’87, there were several tales about professional traders who bought into the market the Friday before the crash, because it had declined too much and was oversold. In fable, “hope” was the last of the creatures let out of Pandora’s box."

With this in mind, we show below a handful of North American energy stocks that are locked in persistent downtrends. Needless to say, we would not recommend attempting to bottom fish among these companies.

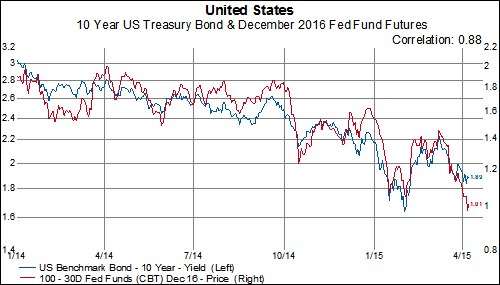

Not even a month ago, we wrote about how it looked like the market was pricing in two rate hikes in 2015 and four in 2016. Well, apparently a lot has changed (at least regarding expectations) since then. The December fed funds futures is only pricing in about one hike from the current effective fed funds rate. Fed fund futures are pricing in a 36 basis point fed funds rate for the end of 2015. This is about half the level that the market expected for most of 2014.

Unsurprisingly, 2016 fed funds rate expectations have fallen sharply as well. The market is now only pricing in a fed funds rate of 101 basis points by the end of 2016. This implies the market expects only 2 and half rate hikes in 2016. So we have gotten to the point where the market expects the fed funds rate to only be 20 basis points higher by the end of 2016 compared to where the market expected in September 2014 for the fed funds rate to be by the end of 2015. Rate hike expectations continue to be pushed back.

The spread between junk bonds and 10-year treasury on 6/23/14 hit a very narrow 222 basis points. At that time, the S&P 500 was trading at 1962. Since then the junk bond spread widened to over 5% in December and currently stands at 415 basis points. The S&P 500 has continued to climb nearly 6% higher.

Junk bonds have also widened out against AAA corporate bonds. While the absolute difference between Junk and AAA spreads is tame (261 basis points), Junk bonds are nearly 125 basis points wider relative to AAA corporates than they were last June.

A lot of this has to do with the continuation of a 30+ year trend in AAA yields. AAA bond yields are basically at all-time lows. Same is true for BBB yields

Long-term municipal bond yields are pretty much at the lowest levels since the mid-1960s.

US 10-year treasury yields are only about 40 bps below all-time lows. Compared, to France and Italy, US yields look downright buoyant. 20-year and 30-year treasury yields are at all-time lows as well.

Regional leadership trends have changed recently in the global equity market. So far this year, in USD terms, Developed Asia-Pacific is the best performing region in the developed world, with Europe second and North America last. In the following tables we show regional performance by sector. We equal weight all the stocks in the sectors and region to remove market-cap related distortions.

MSCI Asia-Pacific

Driven by Japan, Asia-Pacific health care and consumer staples have been the two best performing sectors this year. There are four sectors in Asia-Pacific that have outperformed the best performing sector in Europe.

MSCI Europe

While consumer discretionary has led in Europe, Asian consumer discretionary stocks have actually performed better.

MSCI North America

Health care continues to lead market performance in the US and is actually the only North American sector to outperform the MSCI World index YTD.

Turning to aggregate developed world performance, we can see that leadership is still in the growth counter-cyclical health care and consumer staple groups. Among the cyclical sectors, consumer discretionary and technology are the only two that are outperforming the MSCI World Index.

USD based investors should be wary of Canadian banks. Canadian banks have taken a beating in 2015 and the near-term trend doesn't look to be abating anytime soon. The average USD performance of a Canadian bank year-to-date is a "correction" worthy -13%. Meanwhile, the average performance for a US bank is only -4.5% and this is skewed by Bank of America which is down over 13%. The rest of the group is down 2.72% on average.

Canadian Bank Performance

US Bank Performance

Undoubtedly, one of the reasons for the underperformance of Canadian banks has been the recent knockdown of estimates. Over the past six months, FY1 sales estimates have fallen by 10% on average and FY1 EPS estimates have declined by 13.1%. FY1 sales growth is expected to be negative for five of the six canadian banks and FY1 earnings growth estimate is expected to be significantly negative for all six. FY1 earnings growth is expected to decline by nearly 6% on average.

Change In FY1 Sales Estimates

Change In FY1 EPS Estimates

Sales Growth Expectations

Earnings Growth Expectations

Unfortunately, the recent decline hasn't brought down prices enough to make a truly compelling valuation argument. All the Canadian banks are trading at double-digit P/E ratios and over 2x sales and at least 1.4x book value. Two of the US banks (Citigroup and Bank of America) trade below book value and the highest P/B ratio of any US bank is only 1.8x.

Current Valuations

Lastly, the technical outlook isn't supportive currently. In general this is relative low volatile group and has tended to trade in line with the market. However, every single stock is breaking down and look to be squarely in a downtrend. Unfortunately, these stocks look to be in the early innings of what could be a multi-year trend of underperformance.